Private Wealth Market Commentary: Dispersion, Discipline and Opportunity

March 9, 2026

by Bradley Wallace, CFA®

Markets are off to another volatile start this year, a feeling similar to 12 months ago but with a different set of culprits. Last February, investors were facing significant uncertainty around unprecedented trade policies, sending equity markets down nearly 20% in less than two months.

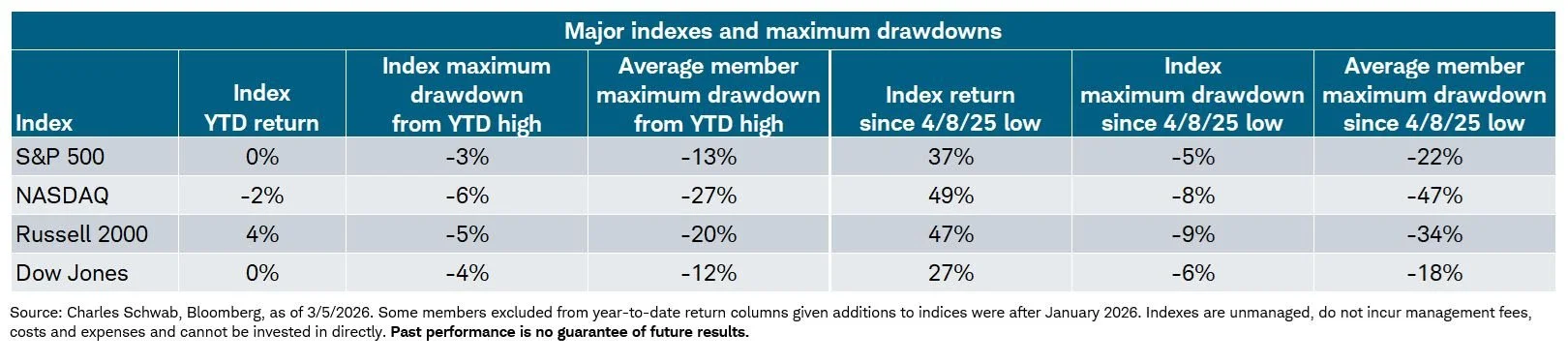

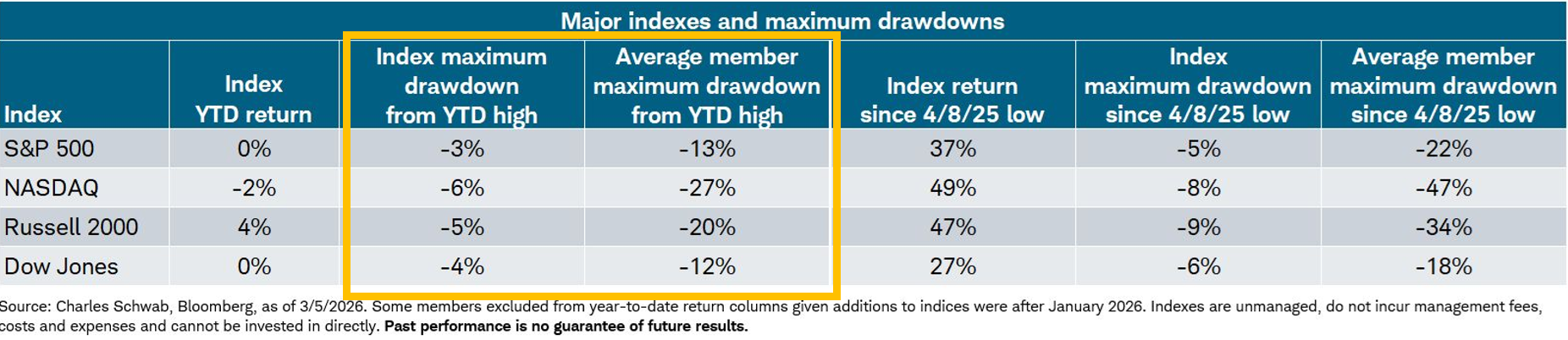

These periods of uncertainty and volatility are difficult for any human to stomach. But for the dispassionate investor, these bouts of dislocation can present years of value-add opportunities in a matter of weeks. Continuing with last year’s example, equities recovered nearly as quickly as they fell, rewarding those who were able to apply discipline and diligence in an otherwise uncomfortable investing environment. As shown in the up-to-date table below, major U.S. equity indexes have returned between 27%-49% since their April 8th low less than a year ago.

Over the long-term, volatility and uncertainty are simply the price of admission for potentially higher investment returns. Simple, not easy. The ability to capitalize on these periods of dislocation rests on an investor, or manager’s, patience, preparation, and awareness of those environments that favor active management.

When Active Management Adds Value

Active management is broader than mere stock picking. Active management, specifically within private wealth, entails risk management, strategic and tactical allocation adjustments, security selection, as well as tax and liquidity management. But even within asset management, which includes manager and security selection, there are certain market environments that present opportunities for active investment managers. More specifically, periods of elevated dispersion – in both performance and valuations – have historically created a broader opportunity set for disciplined active managers.

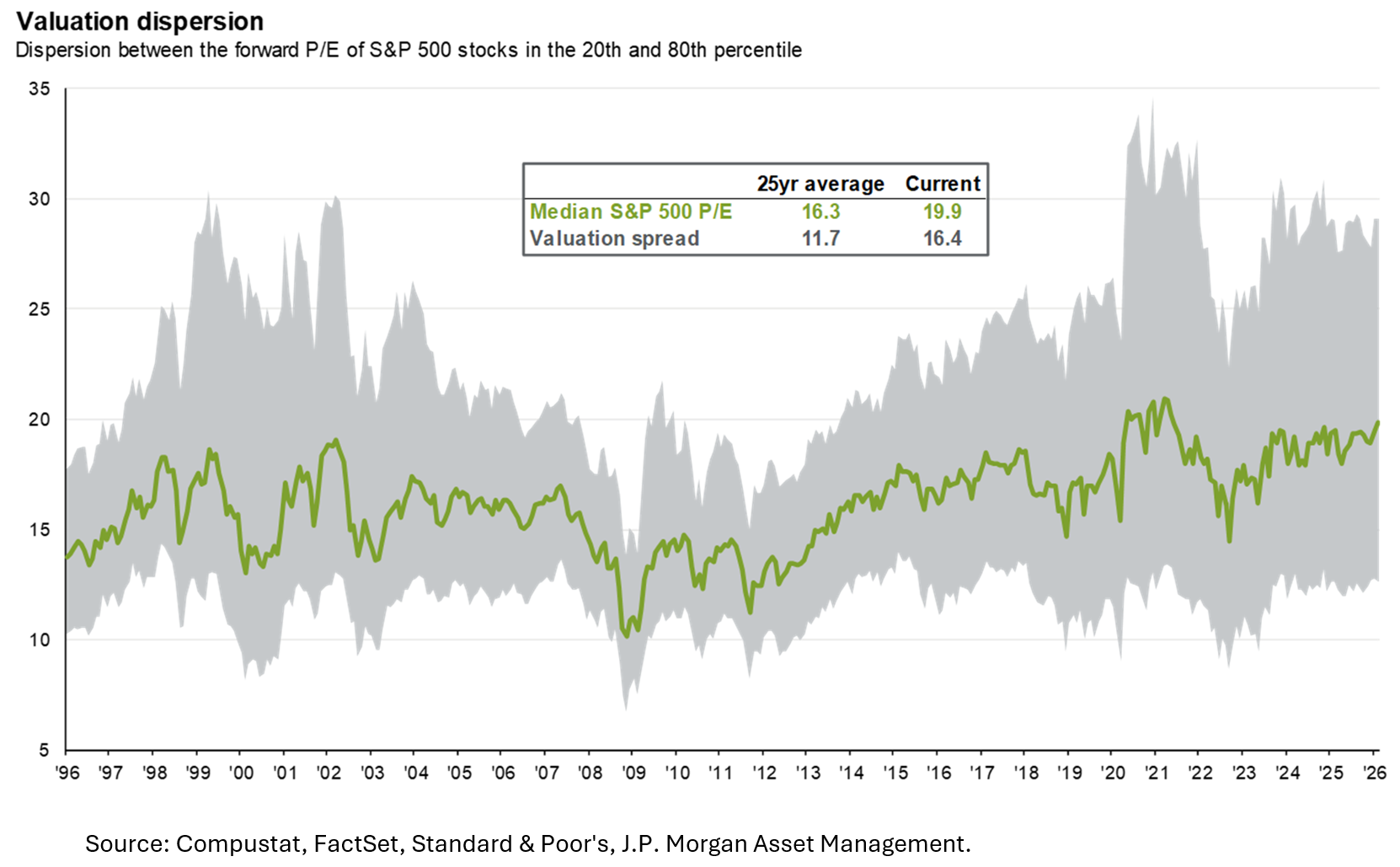

The key for asset managers, however, is recognizing when these environments exist and maintaining the fortitude, diligence and versatility to capitalize on them while they last. By some metrics, it seems as though we are in such an environment today, as can be seen in the adjacent chart from JPMorgan Asset Management, which illustrates the current level of valuation dispersion within the S&P 500.

First, what is dispersion and why do certain market environments present higher (or lower) levels of dispersion than others? Below are two definitions of dispersion as it relates to assets; one that is understandable and another for those who already have a human name for their Agentic AI system:

How big the gap is between the winners and the losers (or most expensive to least expensive) within a market.

The degree of variation in the returns of a portfolio’s components (measured, for example, by the cross-sectional standard deviation of asset performances during the relevant time period)

Example: Imagine a classroom where students take the same test. If everyone scores between 88 and 92, the results are tightly grouped together and the level of dispersion among scores is low. On the other hand, if some students score 98 while others score 55, the results are spread far apart and dispersion is high. Markets work similarly - if most stocks go up or down by roughly the same amount, dispersion is low; but if some stocks are experiencing extraordinary returns while others are going sharply in the other direction, dispersion is high.

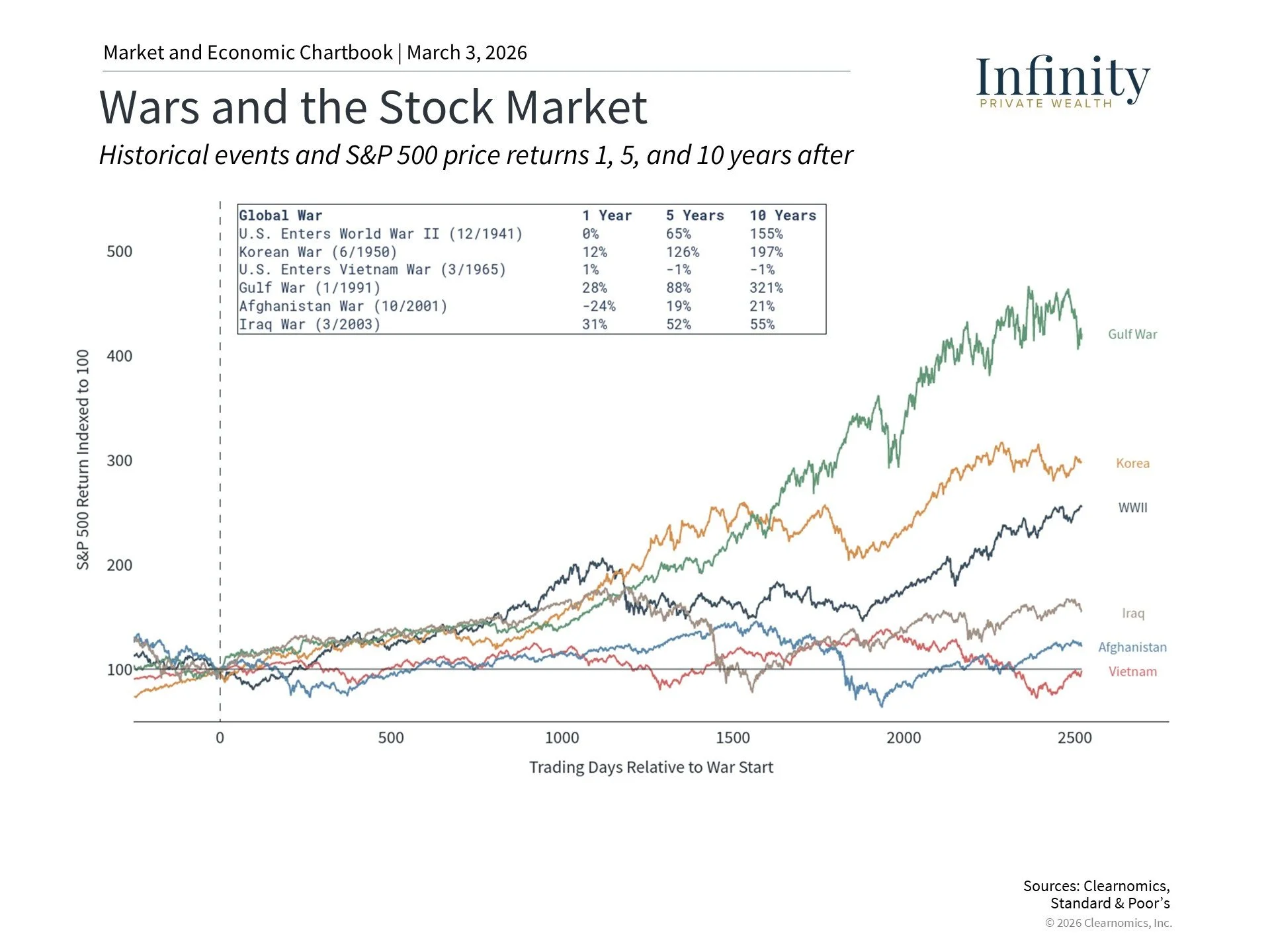

Second, what causes higher levels of market dispersion? In a word, uncertainty. Periods of high dispersion tend to surface when uncertainty – whether economic, technological, or geopolitical – rises. Currently, investors are contending with the uncertainty of all three of these factors. We’ll write more about these issues in our Q1 market update in a few weeks, but for now, amid a bout of volatility seemingly related to geopolitical uncertainty, it’s worth highlighting the below chart as a reminder for long-term investors to maintain perspective.

History of High-Dispersion Periods

Now that we covered what market dispersion is and what influences it, we can look at history to see how different levels of market dispersion have translated into value for active investment managers. During periods of low dispersion – where every stock or other asset moves in tandem – the opportunity to add value narrows, which we have seen in large part over the nearly two-decade period that followed the 2008-09 Great Financial Crisis. But after 2020, markets have become much less synchronous and much more disconnected underneath the surface. History provides empirical evidence for these higher-dispersion periods as well.

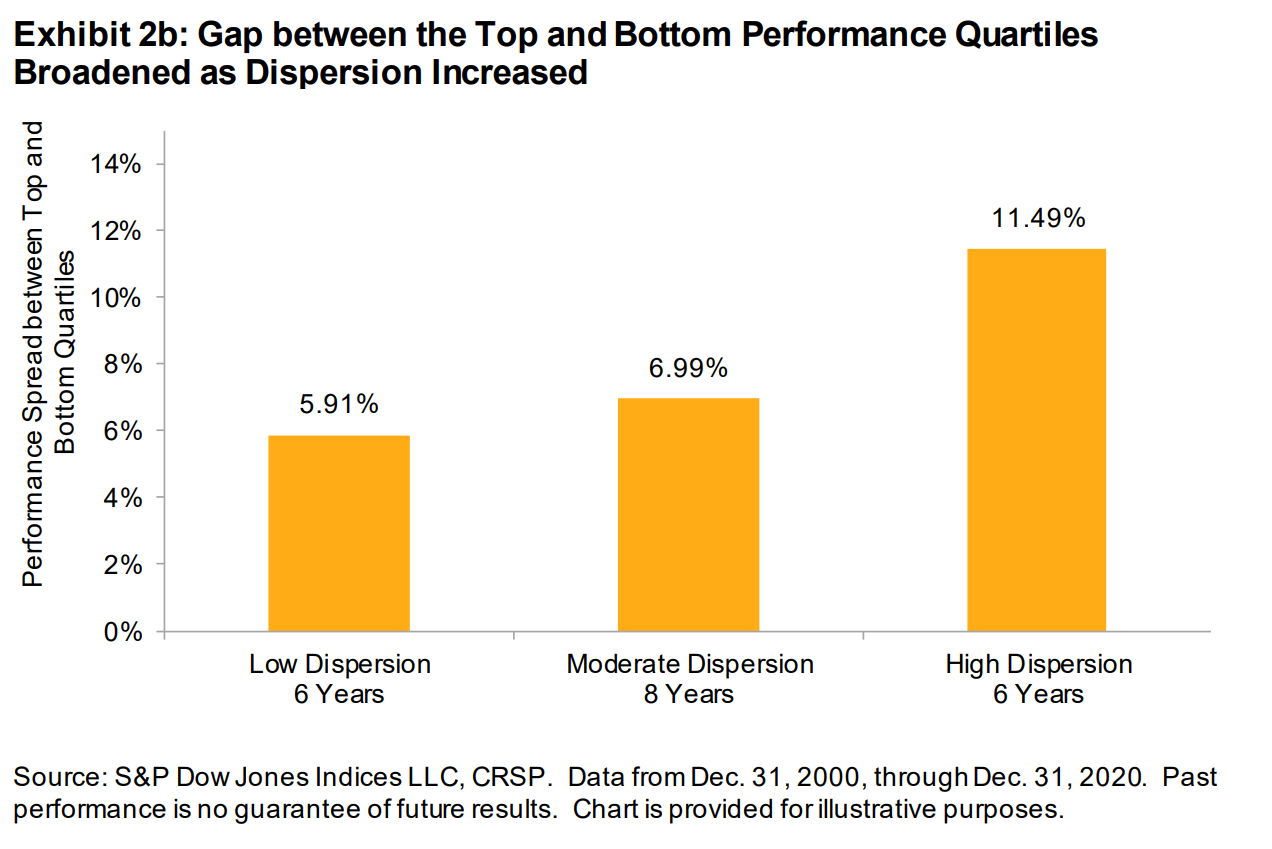

Looking at research from S&P Dow Jones Indices, over the 20-year period from December 2000 to December 2020, the performance gap between top quartile managers and bottom quartile managers was 11.5% in high dispersion years and nearly half that (5.9%) in low dispersion years. For active managers and investors, recognizing when these periods of opportunity are present is the first step in being able to take advantage of them. Second is maintaining the discipline and dispassion to act prudently and decisively. Howard Marks put it best in his 2001 memo: “You can’t predict. You can prepare.”

As we examine the current environment, let’s revisit the table presented earlier. In the highlighted columns below, we can see the variance between index-level drawdowns year-to-date relative to the average member (individual stock) drawdown. Among the four major indexes listed, the average drawdown from its YTD high has been about -4.5%, while the average underlying member drawdown has been closer to -18% from its high over the same period.

In other words, the potential to add value by looking “under the hood” has been ripe this year. On the flip side, prudent risk management has also become increasingly more important. When this happens, there can be greater opportunity for active managers to differentiate results, both in terms of risk-adjusted returns and outright relative performance, compared to a passive index.

Bottom Line

In asset management, opportunities to add long-term value are born when dispersion meets discipline. Dispersion within capital markets often comes from dislocation when uncertainty rises and markets become irrational. Managers who maintain perspective, act with prudence and lead with stewardship are often those best positioned to add long-term value.

At Infinity Private Wealth, this is foundational to our investment process: preparing in advance for when markets become dislocated, and acting with discipline when opportunities appear. We believe long-term investment success is less about predicting markets and more about being prepared when dispersion creates opportunity.